Negotiating the Rapids of Arctic & Alaska Oil and Natural Gas Reserves

This photo shows the aerial view of the Trans-Alaska oil pipeline and Dalton Highway, Kanuti National Wildlife Refuge. (Photo: Steve Hillebrand/Wikimedia Commons)

There are a number of challenges in aggressively pursuing oil and natural gas exploration. However, none of the Arctic nations have slowed down their quest. Even the non arctic-nations, geographically far away from the region, appear anxious to reap the benefits. In this article you can read Dr. Ashok K. Roy og Dr. Shiva Hullavarad opinion on the matter.

“You can never cross the ocean until you have the courage to lose sight of the shore”.

Christopher Columbus

“In the afternoon they came unto a land

In which it seemed always afternoon.

All round the coast the languid air did swoon,

Breathing like one that hath a weary dream.”

Alfred, Lord Tennyson

Three major events occurring between 2006-2008 depict the increasing interest for access and control of oil /natural gas resources in the Arctic and its major passages. These three events are: the opening of the Northwest-East passage through the Bearing Sea due to a decline in sea ice; oil prices reaching $147 a barrel causing concern that the current global oil production will not be able to meet demand from the emerging markets of China, India, and Brazil; and Russia planting a deep-sea flag – as a strategic signal to the world of the importance of Arctic to the leadership in Moscow. Concurrently in the same time frame, the U.S. Geological Survey estimated that circa 25% of the world’s recoverable oil and natural gas deposits were most likely located in the Arctic.

The recent oil price declines are primarily the result of a price war by Saudi Aramco. According to Yardeni Research, an independent investment strategy and economics research firm, the goal of Saudi Aramco is to maintain its market share by pairing oil output to supply. Another factor contributing to the declining oil prices is supply – higher oil production by the U.S. and Canada (from 0.9 million barrel per day or mbd to 12.7 mbd exceeding Saudi Arabia’s 9.6 mbd and Russia’s- 10.6 mbd in the second quarter of 2014). Demand, on the other hand, is not meeting the surplus due to a slower growth rate in advanced economies. Strong declines in commodity prices typically signify a supply-demand imbalance. As to how low the oil prices can go may depend on how much China’s economy slows down as the world’s largest consumer of oil. Falling oil prices could prove an advantage for Mexico since its new oil costs only circa $45 a barrel which is well below the Texan crude; and the proposed 1,000 mile natural gas pipeline from Los Ramones to Texas may also spur global firms to lose interest in the more costly Arctic. Goldman Sachs estimated in mid-2014 that U.S. shale producers will need about $85 a barrel to break even.

It must be noted that there are a number of challenges in aggressively pursuing oil and natural gas exploration. First, the ramifications of an environmental impact in the event of a major oil spill will have to be considered. Second, because of inadequate geological maps, patchy communication systems, and polar icecap melting, iceberg movements become uncertain and unpredictable. Third, the lack of transportation infrastructure to move the extracts from the drilling sites to the processing plants poses a challenge. Finally, the extreme cold weather presents challenges in a number of areas.

Interestingly, despite all these potential challenges none of the Arctic nations (U.S. Canada, Russia, Norway, Iceland, Greenland, and others), have slowed their quest for oil exploration or natural gas reserves and infrastructure development. Even the non-arctic nations that are geographically far away from the region (China, South Korea, India, Italy, Singapore) have shown interest and appear anxious to reap the benefits. As a result, the Arctic Council has granted these nations an observer status. There is a flurry of resource development activities. For example, in Alaska scenario planning has been applied to marine shipping, climate change, port site selection, and resource development issues.

The Arctic environment is changing rapidly, especially with regard to the erosion of the coastlines from storm surges, early breakup and late freeze of ice and shifts in density; and the composition of the Arctic flora and fauna. Over the last five decades, according to the Arctic Climate Impact Assessment Report the thickness of the Arctic ice and the spread have been declining at an annual average rate of 3.7%. At this rate of decline, theoretical models forecast that the Arctic will be completely free of ice by 2040. An ice free land or reduction of hard ice on the high seas will open new opportunities for oil and natural gas production (e.g., from longer exploration seasons) as well as transportation (e.g., from maritime transportation and summer-time trans-Arctic shipping that takes advantage of the shorter distance between Asia and Europe). There will be socioeconomic consequences as the Arctic and the adjacent subarctic seas supply food for indigenous peoples whose traditional way of life and culture are affected by the prevalence of open water. Furthermore, the fragile Arctic ice might move at a greater speed with potential risks to off-shore/ on-shore oil rigs and vessels (e.g., as was experienced by Terra Nova, a large oil field located about 230 miles off the coast of Newfoundland); and roads, runways, pipelines, harbors, and homes all will become more vulnerable to effects of warming in permafrost-rich regions.

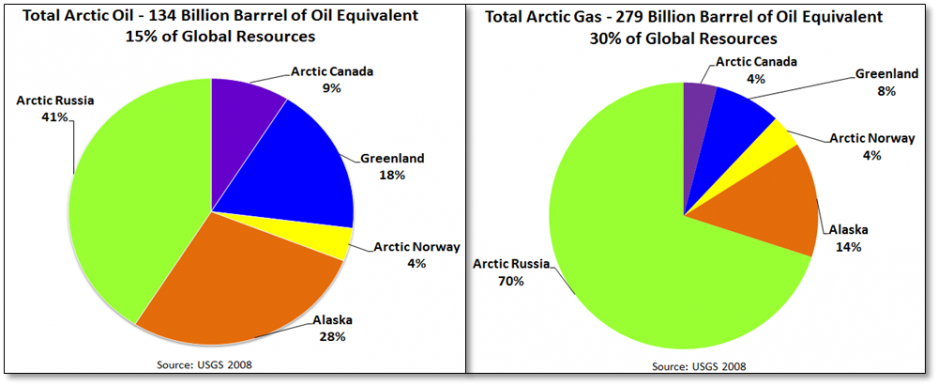

Oil and natural gas companies are likely to take higher risks due to guaranteed returns on their investments in the exploration of these reserves from the region due to its low political risk as measured by the Political Risk Services Group Index (Canada’s index is 94 as compared to, say, Iran’s index of 45: note that higher the index, lower is the political risk).It is estimated that the Arctic has one of the largest hydrocarbon reserves in the world. Notably, Russia, Greenland, and Norway alone hold 82% of the total Arctic gas resources with the remaining 18% split between the U.S. and Canada. Interesting, Russia, Greenland, and Norway account for 63% of the total Arctic oil resources with the remaining 37% split between the U.S. and Canada (Figure 1). The U.S. Energy Information Administration (EIA) estimates that in the next 25 years, the overall world consumption of oil and natural gas will increase by 20 % and 50% respectively. Based on this forecast, it is obvious that the oil and natural gas resources in the Arctic will play a significant role in geopolitics (e.g., in November 2014, to stem the slide in Russia’ exports from oil prices, Russia signed a deal with China to export gas from Siberia via new pipelines in order to replace Europe as its main export market).

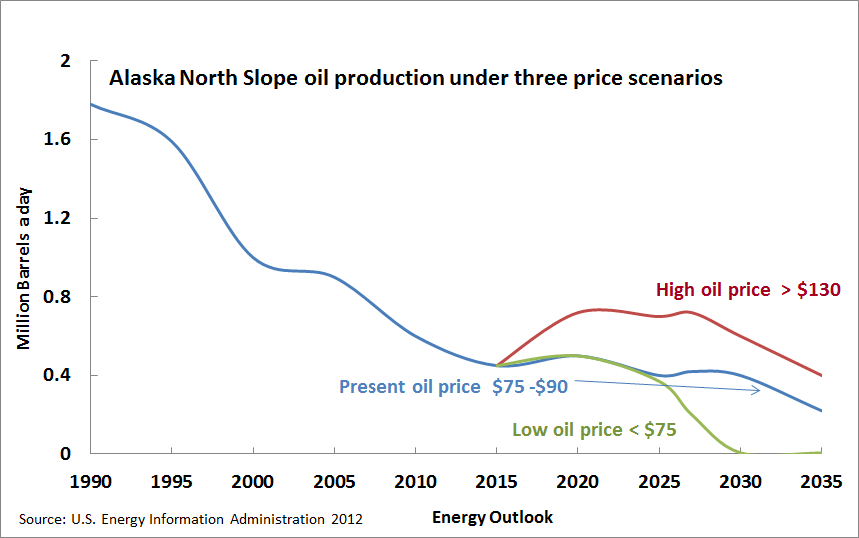

Figure 2

There might also be operational issues with the declining oil supply flowing from North Slope to Valdez. According to the Alyeska Pipeline Service Company estimates low crude oil flow rates through the TAPS below 600,000 barrels per day might lead to technical issues (e.g., pipeline corrosion by potential water drop out from crude oil, ice formation, wax precipitation, deposition and displacement of buried pipelines from soil freeze and thaw as pipeline operating temperatures decrease).

The Arctic will continue to be a focus and will be a major hub for operations for oil and gas companies, arctic and non-arctic nations, and environmental groups due to the reasons enunciated earlier in this article. A number of factors make the Arctic attractive (low political risks, most arctic nations belong to the western capitalist economies, entrepreneurial communities driven by aggressive local and federal government business-friendly policies). Some oil and gas companies have formed consortium to explore the Arctic and leverage each other’s capabilities for resource optimization. Russia, which holds the largest reserves of Arctic oil and natural gas, has nationalized its energy sector. As a consequence, global political and economic trends are less likely to impact Russia’s aggressive strategy in resource exploration and market share. This may force other Arctic nations to follow suit and pave the way for a busier Arctic passage. Needless to say, Arctic nations have been granting exploration licenses to oil companies who have invested approximately $5 billion in just the last decade. The Arctic serves as a backup for the oil companies’ long term supply strategy. There are also bilateral collaborative efforts through government/non-government agencies addressing the various issues of Arctic resource development ranging from physical infrastructure, logistical and operational support, and multilateral research opportunities to investments. The U.S. Arctic Research Commission, in its recent white paper on oil spills in Arctic, recommends future work in areas such as: oil spill response technologies for cleanup and recovery of oil, data management tools and long term effects, thereby providing a clear roadmap for strategic development of natural resources.

In coda, at the confluence of smart resource extraction, hidden riches, and the preservation of pristine landscape, stands the Arctic as an enigmatic and mystic place for the future.

Dr. Ashok K. Roy is the Vice President for Finance & Administration/Chief Financial Officer of the University of Alaska System & Associate Professor of Business Administration at UAF.

Dr. Shiva Hullavarad is the Enterprise Content Management administrator at the University of Alaska System. Dr. Hullavarad has graduate degrees in physics and in business administration, and has authored 70 publications.